Future trading is a crucial activity for the economic development of a nation. To be a successful market approach as speculator,arbitrageous, trader investornor hedger one must have adequate information and a proper understanding of the futures market

It is essential to understand how the futures market works and how the price of future contracts relates to the spot price because futures are useful to the market participants only if future prices reflect information. About the prices of the underlying assets.

Characteristics of future prices

Now we understand the relationship between two prices forward prices are indifferent to the change in the market and spot prices before the maturity because the settlement and delivery of the underlying assets are to be executed at the time of expiration. The change of default may be greater in a forward contract than in a future contract which is closed through the clearing house and settled daily.

We will analyze much about future prices, volatility of future prices, and ba sis. Theories of the future price CAPM model.The theory of normal backwardation.

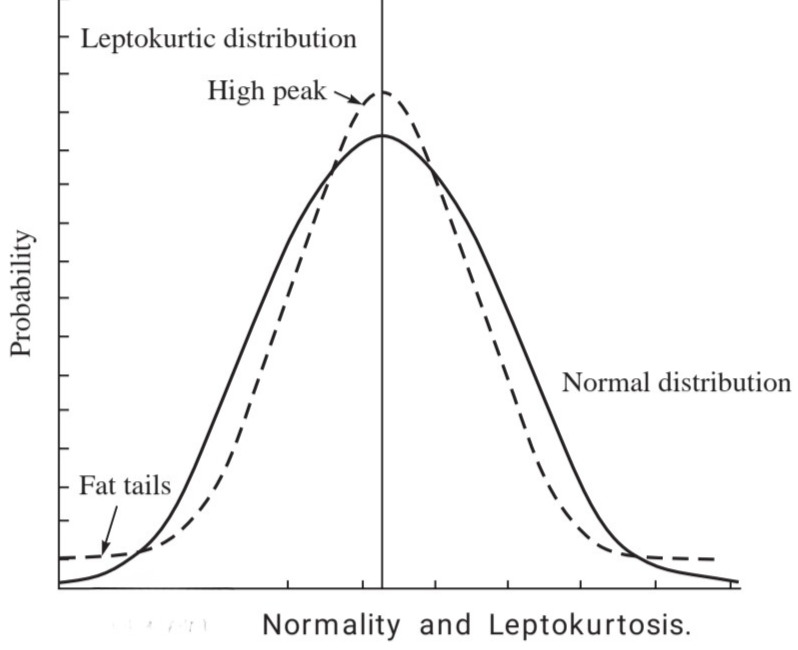

Distribution of future priceThis article analyzes how future price distributed, and most of statical test conducted on future prices rely on the assumption that the underlying price changes are normally distributed. But lots of studied have noticed that the future price are not normally distributed but lots of studied have noticed that the future price are not normally distributed in general ,rather it is leptokurtic which means the tendency for a distribution to have too many extreme observation observation relative to a normal distribution. Now some explanation of normal distribution and leptokurtic distribution.

Normal distribution-> Assume that asset returns are perfectly symmetrical around the average. A statistical distribution that features a higher more pointed peak around its mean and thicker, heavier tails compared to a standard normal distribution.

Leptokurtic distribution- A leptokurtic distribution is a statistical probability that features a sharp tall peak and feat (heavy) tails when compared to a normal (bell-shaped) curves.

In finance and risk management, financial markets and assets return are frequently leptokurtic traditional risk models that assume normal distribution often understimate the probability of severe market crashes windfalls